CONSUMER REPORTS URGES HOLIDAY SHOPPERS NOT TO BUY WARRANTIES

by Amanda Garcia

Although in-store electronics shoppers are more likely to buy extended warranties than online shoppers, these purchases are “bad investments” for consumers, according to a recent survey from Consumer Reports.

Save Your Holiday Budget By Avoiding Extended Warranties

“In past surveys, we’ve found that the vast majority of repairs are made while items are still covered by a factory warranty and that extended warranties typically protect, at relatively high cost, against a very low risk of a catastrophically expensive repair,” Glenn Derene, electronics team leader at Consumer Reports, wrote in the survey. “And bear in mind that buying items with some credit cards extends warranties at no additional cost.”

With so many Black Friday deals and commercials bombarding shoppers throughout the month, avoiding the purchase of an extended warranty can put some extra cash back into your savings account and holiday budget.

One way for holiday shoppers to save on electronic purchases and avoid the need for extended warranties is to buy from reliable brands with models that last for many years, all the while following the manufacturer’s usage and maintenance recommendations.

Extended Warranties Remain Huge Source of Profit for Retailers

Sometimes it’s hard to say no to a salesperson who says tacking a few hundred dollars onto your $1,200 television purchase will protect your investment in the long run. However, many service plans and extended warranties cost more than what they would help consumers recover, and many also have fine print terms and limits that could disqualify your claim.

“Warranty prices have inched up over the years, just as the costs of the devices they cover are trending downward,” said Carmi Levy, an independent technology analyst, in an interview with Yahoo! Shopping. ”When laptops cost $1,500 and the warranties went for $150, it was like cheap insurance. Now, average laptop prices are closer to $500, and warranties can go for about $300.”

Nowadays, many electronics retailers receive two-thirds of an extended warranty as simple profit while the rest is covered by a third-party insurance company responsible for providing coverage on the electronic device.

GAS PRICES DROP TO RECORD LOWS AS HOLIDAYS APPROACH

Photo credit: meddygarnet

With the national average price of gasoline recorded at $3.18 a gallon yesterday by AAA, 26 cents below the same day last year, gas prices in the United States are trending downward to their lowest levels in almost 33 months.

Low Price of Gas Due to Domestic Inventory Surplus

AAA also predicted the national average price of gas will drop close to $3 a gallon by the end of the year thanks to declining seasonal demand, lower crude oil prices and abundant supply.

U.S. oil refineries are producing more gasoline than drivers need, especially within the Midwest, driving the price of gas down and allowing a little extra cash to flow back into savings accounts. As the extra fuel is placed in storage tanks across the country, domestic gasoline inventories have increased by almost eight million barrels since last November, according to the Energy Information Administration.

“Refiners are still making money on diesel, but gasoline is almost a by product,” Sarah Emerson, managing director of consulting firm ESAI Energy, said in an interview with The Wall Street Journal.

Holiday Travel Demand Could Affect Cheap Gas Prices

If demand increases along with consumption due to holiday travel plans, prices can rebound quickly. However, since refiners are still producing substantial quantities of gasoline, it would take weeks of strong demand to deplete the surplus and drive up the price of gas.

Drivers in Texas, Louisiana, Missouri and three other states are currently paying cheap gas prices of less than $3 a gallon on average, while Louisiana currently boasts the cheapest price of gas at $2.81 a gallon. Additionally, drivers in Iowa, Indiana, Minnesota, Ohio and seven other states only have to pay $3.10 or less per gallon for gas.

WHAT IS A CREDIT UNION?

by Amanda Garcia

Banking isn’t just for banks. Another type of financial institution that millions of people use every day is called a credit union. Credit unions operate similarly to banks with a few key differences which might make a credit union the perfect option for you.

What Is a Credit Union?

A credit union is a not-for-profit financial collective, and members of credit unions are also considered part owners. Rather than operating with the goal of making a profit and providing value to shareholders which are the primary objectives of banks, credit unions make their members the top priority.

Extra earnings that don’t go to overhead and administrative costs are returned to members in the form of higher interest rates on deposit accounts like savings and CDs, as well as lower rates on loans for cars, homes and more.

Benefits of Credit Union Loans and Accounts

Credit union loans are sometimes available when loans from larger, nation banking chains aren’t. That’s because credit unions exist to support the local community so they’re often more likely to lend within it, especially if the loan amount is on the small side. Additionally, credit union loans tend to have much lower rates — whether you’re interested in financing a home purchase or need a loan to buy a car, credit union loans are very competitive in terms of interest rates and features.

The same is usually true of deposit accounts from credit unions. Because a credit union member is also part owner of the institution, he or she will earn dividends (interest), which are generally much higher than the interest offered on major bank accounts. This joint ownership is also why credit unions refer to their accounts as “share” accounts as all member owners’ deposits are treated as shares of the organization. |

|

Are Credit Unions Safe?

Don’t let the small town feel of a credit union fool you — credit unions are regulated just like banks, and are federally insured by the National Credit Union Administration, or NCUA (the credit union version of the FDIC), up to federal limits.

Additionally, they aren’t outdated and inconvenient to belong to as is a common misconception. Most credit unions have online banking and other technological services that are on par with major banks, if not better. Plus, credit unions belong to ATM networks so members of one credit union can often use an ATM belonging to any credit union within the network.

How to Join and Find a Credit Union

Every credit union seeks to benefit a particular group of people or organization. There are credit unions for teachers, military, residents of specific cities, and many more. However, that means that in order to become a member of a credit union you must qualify to join under its field of membership.

Membership eligibility is different for each credit union, but there’s often at least one, usually several, that you will qualify to join nearby. One thing that all credit unions require for membership, however, is a small deposit or membership fee and application. Research the credit unions near you to find out if one meets the needs of your specific situation.

The distinctions between a bank and credit union are easily blurred; after all, both offer similar products and services like checking accounts and home loans. However, when it comes to how each operates and the benefits that depositors and borrowers receive, there are vast differences between the two.

Here’s everything you need to know about banks and credit unions to help you decide which kind of financial institution is best for your needs.

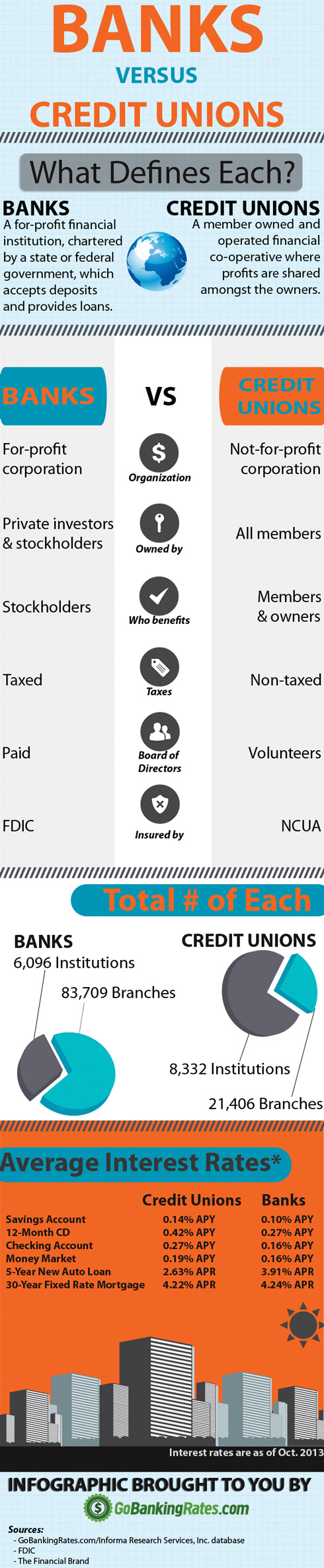

Banks Vs. Credit Unions – By the Numbers

Bank Definition: A for-profit financial institution, chartered by a state or federal government which accepts deposits and provides loans.

Credit Union Definition: A member owned and operated financial co-operative where profits are shared amongst the owners.

Number of Institutions and Branches

| Credit Unions |

Banks |

| • Institutions – 8,332 |

• Institutions – 6,096 |

| • Branches – 21,406 |

• Branches – 83,709 |

Average Interest Rates

| |

Credit Unions |

Banks |

| Savings Account |

0.14% APY |

0.10% APY |

| 12-Month CD |

0.42% APY |

0.27% APY |

| Checking Account |

0.27% APY |

0.16% APY |

| Money Market |

0.19% APY |

0.16% APY |

| 5-Year New Auto Loan |

2.63% APR |

3.91% APR |

| 30-Year Fixed Rate Mortgage |

4.22% APR |

4.24% APR |

Savings products assume a $10k deposit

Source: Informa Research Services, Inc. as of 10/23/13

Sources: GoBankingRates.com/Informa Research Services, Inc. database,

FDIC, The Financial Brand

© 2013 TLC Magazine Online, Inc. |