4 STEPS TO PREVENT MORTGAGE DEFAULT WHEN YOU LOSE YOUR JOB

by Casey Bond

Suppose you lose your job, but still have monthly mortgage payments to make. Unfortunately, few people can keep up with their mortgage payments with only unemployment benefits to rely on. Plus, if your benefits run out before you find your next job, the situation will likely become desperate.

The thought of losing your house is devastating, but know that there are steps you can take to ensure you don’t default on your loan and risk foreclosure in the event you are unemployed.

How to Handle Mortgage Payments When You’re Unemployed

Step No. 1: Review Your Insurance

If you plan in advance, you can insure yourself against suffering through unemployment with various mortgage protection programs offered by insurers. Sometimes home builders even throw in free unemployment insurance to entice you to buy a house from them. Mortgage protection insurance works as follows:

If you lose your job within a specified time after buying the house, typically two years, you will be covered for the full amount of:

• Mortgage payments

• Taxes

• Home insurance payments

You’ll receive this coverage so long as these costs are within the specified limit which generally ranges from $2,000 to $3,000 per month. Unfortunately, no insurance currently available will cover you for the full life of the mortgage (e.g., 30 years), nor will it cover you in the case of extended unemployment. This means job loss insurance should be considered a short term solution.

Step No. 2: Dip into Savings

If you just lost your job, you should immediately take count of all your savings and determine how long you can afford to make mortgage payments before running out of money. Don’t forget to count your severance package, unemployment benefits and any emergency savings you have accumulated while also considering the costs of your other necessities.

If you have enough money to last at least six to eight months, and you feel optimistic about finding a new job, by all means give it a try. Just make sure you move to step No. 3 with at least two to three months to spare before your money runs out.

Step No. 3: Contact Your Lender

Once it looks like you’ll soon be unable to make any more payments contact your lender. Don’t wait until your mortgage is delinquent! The earlier you start this step, the better your chances will be to come out of this on top.

“Almost all lenders are willing to work with homeowners who have a temporary hardship,” Greg Cook of FirstTimeHomeBuyersNetwork.com said. “The first call, before they miss a payment, should be to the customer service department of their current lender and see what arrangements can be worked out.”

As long as you reach out to your lender before you miss any payments there is a good chance a deal can be struck.

“The most commonly used program is forbearance, a deferment of the missed payments for a set period of time,” Cook said. “Those payments [might] either be added to the end of the loan or amortized over a period once the hardship

is removed.”

Step No. 4: Seek Help from the FHA

If you’ve become delinquent on your mortgage seek out programs for homeowners in your situation. For example, certain mortgages qualify for a “partial claim” arrangement with the Federal Housing Administration which provides you an interest free loan from the government that covers all your missed payments up to 12 months. This loan does not have to be repaid until you sell the house or pay off the mortgage.

The partial claim arrangement is a great deal, so you should definitely go for it if you qualify. Furthermore, you can continue negotiating with the lender at the same time.

Regardless of which option you choose, it’s best to speak with a mortgage expert and determine the best course of action, as well as any repercussions, before moving forward.

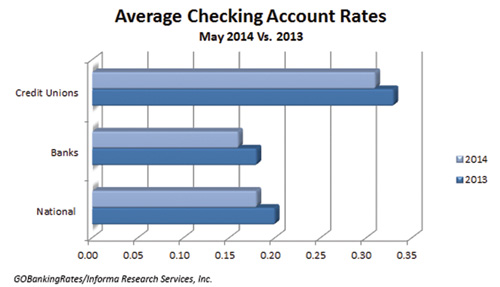

CREDIT UNION CHECKING ACCOUNT RATES ARE DOUBLE THOSE FROM BANKS

Checking account rates have finally begun to trend upward signaling a shift from the steady declines we’ve experienced since 2008 though we haven’t seen too much movement since April.

The national average grew by one basis point month over month to 0.18% APY. While this is still a 0.02% decline from May of last year, the slight increase is a good sign we’ve experienced rock bottom deposit rates and are on the way to recovery.

Credit unions continue to lead financial institutions in offering the highest yields on average with 0.31% APY versus 0.16% APY at banks. Even so, the very best checking account rate is still found at Home Federal Bank which provides customers 4.00% APY (more than 22 times the national average).

Best Checking Account Rates – May 2014

Below are the highest checking account interest rates currently available from U.S. banks and credit unions, according to our database.

| Institution |

Location |

Product |

APY |

| Home Federal Bank |

Shreveport, LA |

Smart Rewards Checking |

4.00% |

| JD Bank |

Lake Charles, LA |

Kasasa Cash |

3.25% |

| Frontier Bank |

Rock Rapids, IA |

Kasasa Cash |

3.05% |

| Community Financial Services Bank |

Benton, KY |

Kasasa Cash |

3.05% |

| Adirondack Bank |

Utica, NY |

eCo Checking |

3.04% |

| American Trust & Savings Bank |

Dubuque, IA |

REWARDChecking |

3.01% |

| The Community Bank |

Zanesville, OH |

Reward Checking |

3.01% |

| Ouachita Independent Bank |

Monroe, LA |

Reward Checking |

3.01% |

| Southern Bank |

Poplar Bluff, MO |

Kasasa Cash |

3.01% |

Sources: GOBankingRates.com and Informa Research Services Inc. (www.informars.com). Although the information has been obtained from the various financial institutions, the accuracy cannot be guaranteed.

All interest rates are accurate as of May 14, 2014. Rates are subject to change at any time at the discretion of individual financial institutions. Additional terms and restrictions could apply. Please verify rates before opening an account.

THE 10 BEST BANKS FOR BABY BOOMERS

Americans age 50 to 68 are some of the most important and influential consumers today though many institutions are failing to meet their unique needs in the banking world.

According to a 2012 Nielsen report, there are presently more than 80 million baby boomers, defined as those born between 1946 and 1964, and it’s projected that half the U.S. population will be age 50 or older by 2017.

Further, a recent Gallup poll found baby boomers make up the largest share of banking customers in the United States with 89 percent currently owning at least one checking, savings, or money market account.

However, according to the report, “While millennials are a hot topic in all kinds of banking strategy meetings, Gallup’s research shows that baby boomers, because of their sheer numbers, are still the largest and arguably the most influential generation. This is a result of its strongest purchasing power with regard to various banking businesses such as retail, wealth management, and even business banking.”

Jason Kincy, marketing director for Arvest Bank, told GOBankingRates, “Most baby boomers are at a stage in life when they require banking convenience that fits their lifestyle and complex financial needs. They value rich checking account options and assistance in financial planning for retirement and beyond.”

Kincy added that in addition to convenience and tailored banking services, “Whether they are preparing to retire or are retired, they want access to financial advisors who can help them maximize their financial decisions.”

Best Banks for the Baby Boomer Generation

Chosen for their retirement and estate planning services, excellent customer service and bank accounts designed for older customers, GOBankingRates identified the best banks for baby boomers in 2014.

1. Citizens Bank – Providence, RI

Citizens Bank will allow anyone, customer or not, to schedule a complimentary financial review with a Citizens Investment Services Financial Consultant even if they are currently a client of another investment firm.

Last year, Citizens was named one of the “Best Banks in America” by CNN Money for “Best Customer Service.” According to the report, Citizens Bank was the only institution in the survey that “had phone reps available 24/7, offered customer service via online instant messaging, weekdays - 9 a.m. to 8 p.m., and had long branch hours - 55 during the week, plus 10 on weekends, including Sundays.”

In fact, the bank has a wide presence for customers who prefer in branch services over mobile banking with more than 1,300 branches and 3,600 ATMs throughout the country.

2. Frost Bank – San Antonio, TX

Frost Bank is home to a host of comprehensive planning tools and resources. These tools include trust and estate planning, the Life Events Planner, and “Directions,” a quarterly newsletter for Frost customers featuring investment news, financial tips and strategies, as well as an exclusive economic outlook by Tom Stringfellow, president of Frost Investment Advisors.

The 2013 J.D. Power Retail Banking Satisfaction survey ranked Frost National Bank highest in the Texas region where the bank performed highest in the product offerings, account activities, fees, account information and facility factors.

Frost is highly accessible to customers through more than 100 financial centers throughout Austin, Corpus Christi, Dallas, Fort Worth, Houston, Rio Grande Valley and San Antonio.

3. Arvest Bank – Lowell, AR

Arvest Bank places emphasis on “customer focused banking,” which means customers enjoy extended branch hours, as well as top tier mobile and online banking.

The 2013 J.D. Power Retail Banking Satisfaction survey ranked Arvest Bank highest in the south central region, noting the bank performed particularly well in the product offerings, facility, account information and channel activities factors.

Arvest also builds customized banking solutions around major life stages and milestones with a focus on investments, home loans, personal banking, retirement planning and

commercial loans.

4. BB&T – Winston-Salem, NC

BB&T offers in-branch meetings to review the needs of those near retirement or in retirement. Customers can review expenses, Social Security and retirement savings with BB&T Investment Counselors.

Further, the bank’s Senior Checking account provides several ways to waive its monthly fee, including when customers set up a monthly directly deposit of $100 or more, maintain an average balance of at least $1,000 per statement cycle, have $6,000 or more in combined deposits across all accounts, or are a BB&T mortgage customer.

Finally, understanding the expenses customers within the baby boomer age range often face, BB&T allows one no-penalty early CD withdrawal for medical emergencies.

5. TD Bank – Cherry Hill, NJ

Known as “America’s Most Convenient Bank,” TD Bank has nearly 1,300 locations along the east coast with longer hours than any other bank, including weekends. The bank also only closes seven days a year.

The TD 60 Plus Checking account offers a low minimum balance requirement of just $250 to waive $10 monthly maintenance fee, free standard checks, a safe deposit box discount on 3×5 boxes where available, free money orders, official bank checks and fee free paper statements.

According to J.D. Power’s 2013 U.S. Retail Banking Satisfaction study, TD Bank ranked highest in the Florida region.

6. Bangor Savings Bank – Bangor, ME

Bangor Savings Bank offers a full Wealth Management division. The Wealth Management Division takes into account individual goals, assets and family needs in order to tailor financial solutions for customers, focusing on investments, retirement planning, trusts/estates and institutional services.

The 2013 J.D. Power Retail Banking Satisfaction survey ranked Bangor Savings Bank highest in the New England region, noting the institution performed particularly well in the product offerings, fees and channel activities sectors.

In March 2014, Bangor Savings Bank was recognized as a J.D. Power 2014 Customer Champion, an elite list of 50 U.S. companies that focus on service excellence.

Bangor Saving Bank is the oldest bank in Maine with a 160 year history of serving the community.

7. Huntington Bank – Columbus, OH

Through its Huntington Wealth Advisors division, Huntington Bank offers a team of experts in private banking, investments, insurance, and trust and estate administration who all work together in one place providing customers a single point of contact for life and income planning, wealth management, trust and estate administration, and more.

Additionally, the 2013 J.D. Power Retail Banking Satisfaction survey ranked Huntington National Bank highest in the north central region, especially in the areas of account information, fees and channel activities.

Huntington is known for low fees on banking products, like the Asterisk Free Checking account that provides a full range of checking features with no maintenance fees, no minimum balance requirements, and free identity theft resolution among other benefits, as well as relationship discounts on home equity, auto and personal loans.

8. Wells Fargo – San Francisco, CA

Presently, Wells Fargo is running its “When people talk, great things happen” campaign, which focuses on face-to-face banking service and encourages consumers to come in and personally speak with a Wells Fargo banker for a “My Financial Priorities” meeting.

The bank also offers Life Management Services to assist older customers and their families with major life transitions. The Life Management Services team works closely with other Wells Fargo specialists including “trust officers, specialists in real estate and closely held asset management, investment managers and private bankers in order to provide comprehensive financial and personal solutions.”

Wells Fargo also provides an online financial education center to help customers navigate the questions and concerns that arise when planning and saving for retirement.

9. USAA – San Antonio, TX

With an extensive Advice Center, USAA provides comprehensive resources and tools for customers facing any number of important financial milestones, such as paying for a child’s college education, planning for retirement and buying life insurance. Additionally, according to Consumer Reports, USAA’s brokerage service was rated highest for overall satisfaction by clients.

USAA membership is open to U.S. military service members, veterans who have honorably served and their eligible family members. In addition to advantages like free financial resources and special savings, membership provides financial benefits for active duty and deployed members specifically.

10. American Savings Bank – Honolulu, HI

American Savings Bank is one of Hawaii’s longest standing financial institutions serving the community for more than 85 years. With over 55 conveniently located branches throughout the state, American Savings Bank offers best-in-class products, extended branch hours and online banking options.

Through its joint marketing agreement with LPL Financial, American Savings Bank offers customers a wide selection of financial planning options through its American Insurance and Investments division.

The bank is also highly involved in its community, committing time and resources to philanthropic giving, volunteerism, education, strengthening families and economic development.

*Investment products are not FDIC insured.

© 2014 TLC Magazine Online, Inc. |